AR models are also known as autoregressive models.

As the name autoregressive implies, it refers to a stochastic process in which the output of the model at time t depends on its own output before time t.

1

2

3

| import statsmodels.api as sm

import numpy as np

import matplotlib.pyplot as plt

|

Create data for AR process

#

Prepare functions to generate data

1

2

3

4

5

6

7

8

9

10

11

12

| def create_ARdata(phis=[0.1], N=500, init=1, c=1, sigma=0.3):

"""Generating AR process data"""

print(f"==AR({len(phis)}), #data={N}==")

data = np.zeros(N)

data[0] = init + np.random.normal(0, sigma)

for t in range(2, N):

res = c + np.random.normal(0, sigma)

for j, phi_j in enumerate(phis):

res += phi_j * data[t - j - 1]

data[t] = res

return data

|

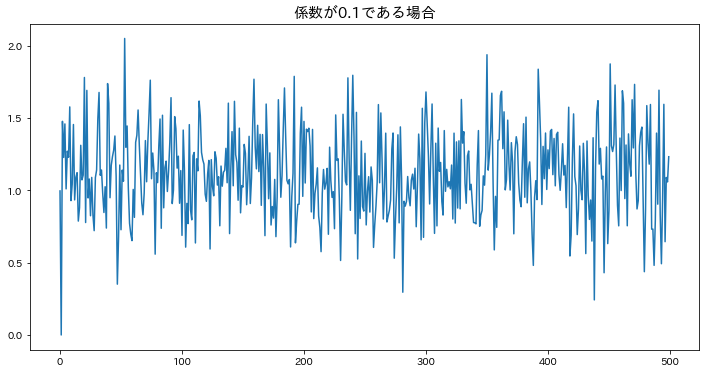

φ < 1

#

1

2

3

4

5

| plt.figure(figsize=(12, 6))

phis = [0.1]

ar1_1 = create_ARdata(phis=phis)

plt.plot(ar1_1)

plt.show()

|

==AR(1), #data=500==

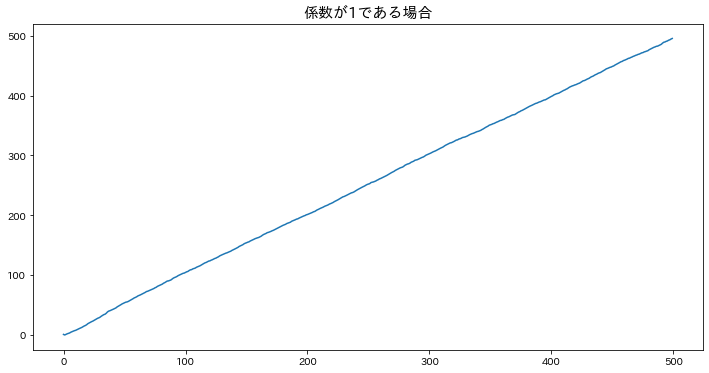

φ = 1

#

1

2

3

4

5

| plt.figure(figsize=(12, 6))

phis = [1]

ar1_2 = create_ARdata(phis=phis)

plt.plot(ar1_2)

plt.show()

|

==AR(1), #data=500==

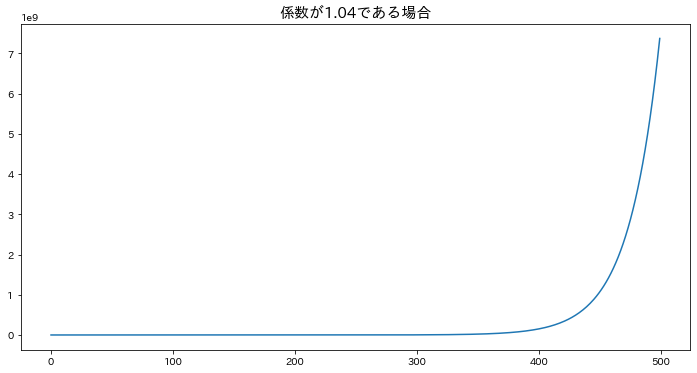

φ > 1

#

1

2

3

4

5

| plt.figure(figsize=(12, 6))

phis = [1.04]

ar1_2 = create_ARdata(phis=phis)

plt.plot(ar1_2)

plt.show()

|

==AR(1), #data=500==

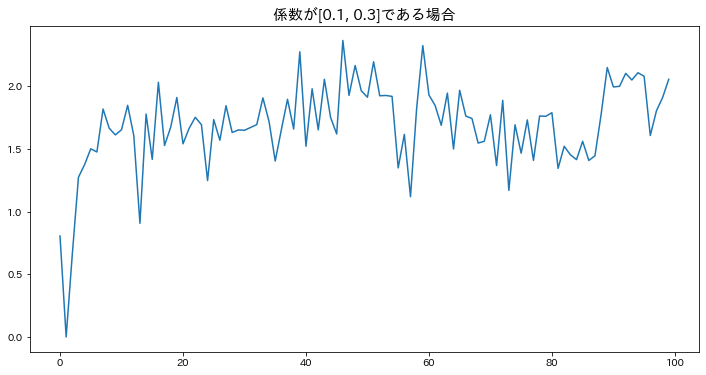

AR(2)

#

1

2

3

4

5

| plt.figure(figsize=(12, 6))

phis = [0.1, 0.3]

ar2_1 = create_ARdata(phis=phis, N=100)

plt.plot(ar2_1)

plt.show()

|

==AR(2), #data=100==

1

2

3

4

5

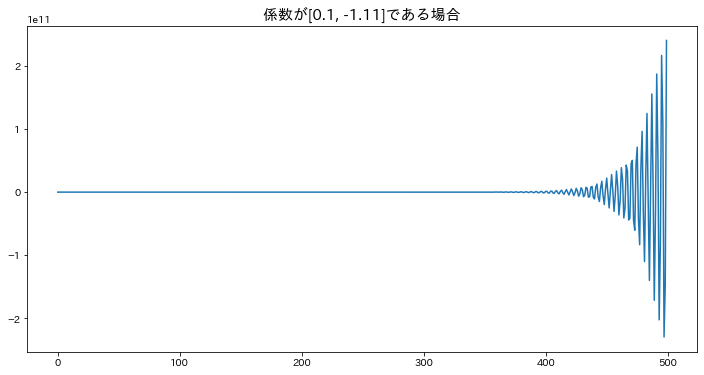

| plt.figure(figsize=(12, 6))

phis = [0.1, -1.11]

ar2_1 = create_ARdata(phis=phis)

plt.plot(ar2_1)

plt.show()

|

==AR(2), #data=500==

Estimate the autoregressive (AR) model

#

1

2

3

4

5

6

| from statsmodels.tsa.ar_model import AutoReg

res = AutoReg(ar1_1, lags=1).fit()

out = "AIC: {0:0.3f}, HQIC: {1:0.3f}, BIC: {2:0.3f}"

print(out.format(res.aic, res.hqic, res.bic))

|

AIC: 231.486, HQIC: 236.445, BIC: 244.124

1

2

3

| print(res.params)

print(res.sigma2)

res.summary()

|

[1.03832755 0.07236388]

0.09199676371696269

AutoReg Model Results| Dep. Variable: | y | No. Observations: | 500 |

|---|

| Model: | AutoReg(1) | Log Likelihood | -112.743 |

|---|

| Method: | Conditional MLE | S.D. of innovations | 0.303 |

|---|

| Date: | Sat, 13 Aug 2022 | AIC | 231.486 |

|---|

| Time: | 01:55:17 | BIC | 244.124 |

|---|

| Sample: | 1 | HQIC | 236.445 |

|---|

| 500 | | |

|---|

| coef | std err | z | P>|z| | [0.025 | 0.975] |

|---|

| const | 1.0383 | 0.052 | 20.059 | 0.000 | 0.937 | 1.140 |

|---|

| y.L1 | 0.0724 | 0.045 | 1.621 | 0.105 | -0.015 | 0.160 |

|---|

Roots | Real | Imaginary | Modulus | Frequency |

|---|

| AR.1 | 13.8190 | +0.0000j | 13.8190 | 0.0000 |

|---|

- MA Process — Stochastic process expressing current value as a linear combination of errors